Portfolio Management in Complex Markets: From Episodic Optimisation to Continuous Transformation

Corporate portfolio management is undergoing a fundamental shift in a volatile and rapidly evolving trading environment. What distinguishes the current landscape is the simultaneous interaction of several disruptive forces; geopolitical fragmentation, regulatory intervention, technological disruption and demographic pressures.

1. A market environment defined by overwhelming complexity and constant pressure

Corporate portfolio management is undergoing a fundamental shift in a volatile and rapidly evolving trading environment. What distinguishes the current landscape is the simultaneous interaction of several disruptive forces; geopolitical fragmentation, regulatory intervention, technological disruption and demographic pressures. The combined effect produces a level of complexity that increasingly exceeds the processing capacity of management teams. Commentators have come to describe this condition as a “polycrisis”: a set of interconnected shocks whose aggregate impact is greater than the sum of its parts.

The consequence for portfolio management is more far-reaching than it first appears. The long-standing assumption that markets can be analysed, modelled and forecast with enough reliability to underpin long-term planning no longer holds in full. The useful life of strategic assumptions is shortening materially, and with it the value of the detailed multi-year plan as a steering instrument. This produces a genuine paradox: complexity has reached a point at which comprehensive analysis is increasingly unrealistic, yet the need for decisive action and active portfolio steering has rarely been greater.

Management teams therefore operate under dual and paradoxical pressure:

Increased uncertainty and ambiguity, which erodes the value of detailed long-term plans

Rising execution urgency, which demands faster and more consequential decisions

Taken together, these pressures reorient the purpose of portfolio management toward dynamic, continuous transformation, away from the static optimisation of a fixed structure.

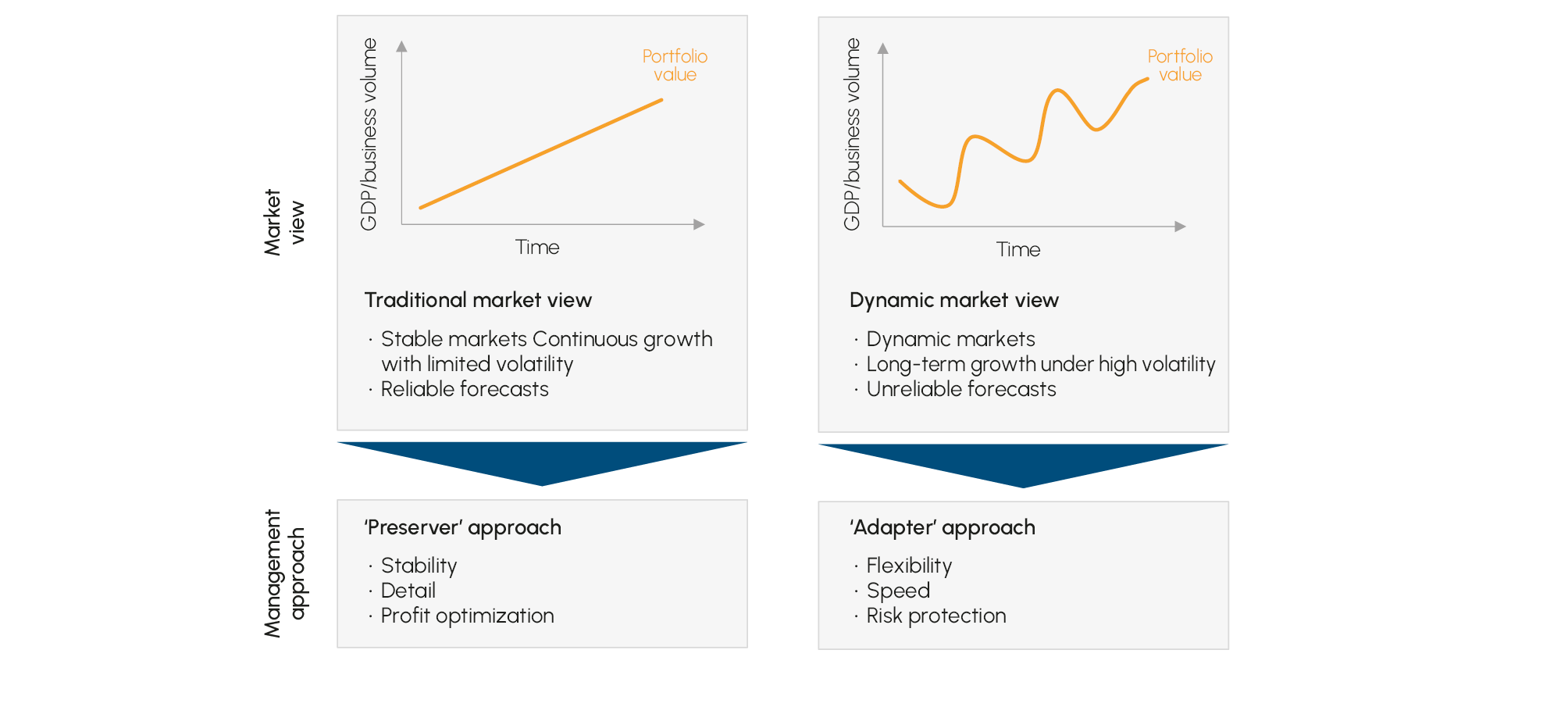

Fig. 1 Adapter vs. Preserver

Source: Interpath

2. Portfolio management and strategy: from preserver to adapter

At its core, portfolio management serves a single overarching objective, namely to keep the composition of the business portfolio aligned with corporate strategy and maximise the strategic fit. This objective has not changed, however the stability of alignment has. Where reconciling portfolio composition and strategy was once a periodic exercise, it has become a continuous and increasingly dynamic task.

Historically, companies could operate in what might be called “preserver mode.” Stable markets allowed strategy to be translated into relatively durable portfolio structures, and management attention could concentrate on efficiency, scale and the long-term optimisation of existing businesses. The portfolio was, in effect, a structure to be refined.

That paradigm is now being complemented, if not entirely displaced by an “adapter” posture. In volatile environments, flexibility, speed and risk management become the dominant strategic imperatives, and the portfolio is considered dynamic and something that continuously reshapes. Amidst constantly changing operating conditions there is a constant need to adapt strategy and recalibrate corporate portfolios in consequence. The shift is already observable, we see leaders prioritising flexibility, speed and risk optimisation, perhaps more so over stability.

The transition is not, however, a binary one. The central leadership challenge requires a dual mindset:

Preserving the stable, cash-generative core businesses that fund the enterprise

While simultaneously adapting the portfolio toward new opportunities, emerging risks (future business) and reshaping it where there no longer is strategic fit (non-core business)

Maintaining a balance between these two is the key challenge of competent portfolio management in the current environment.

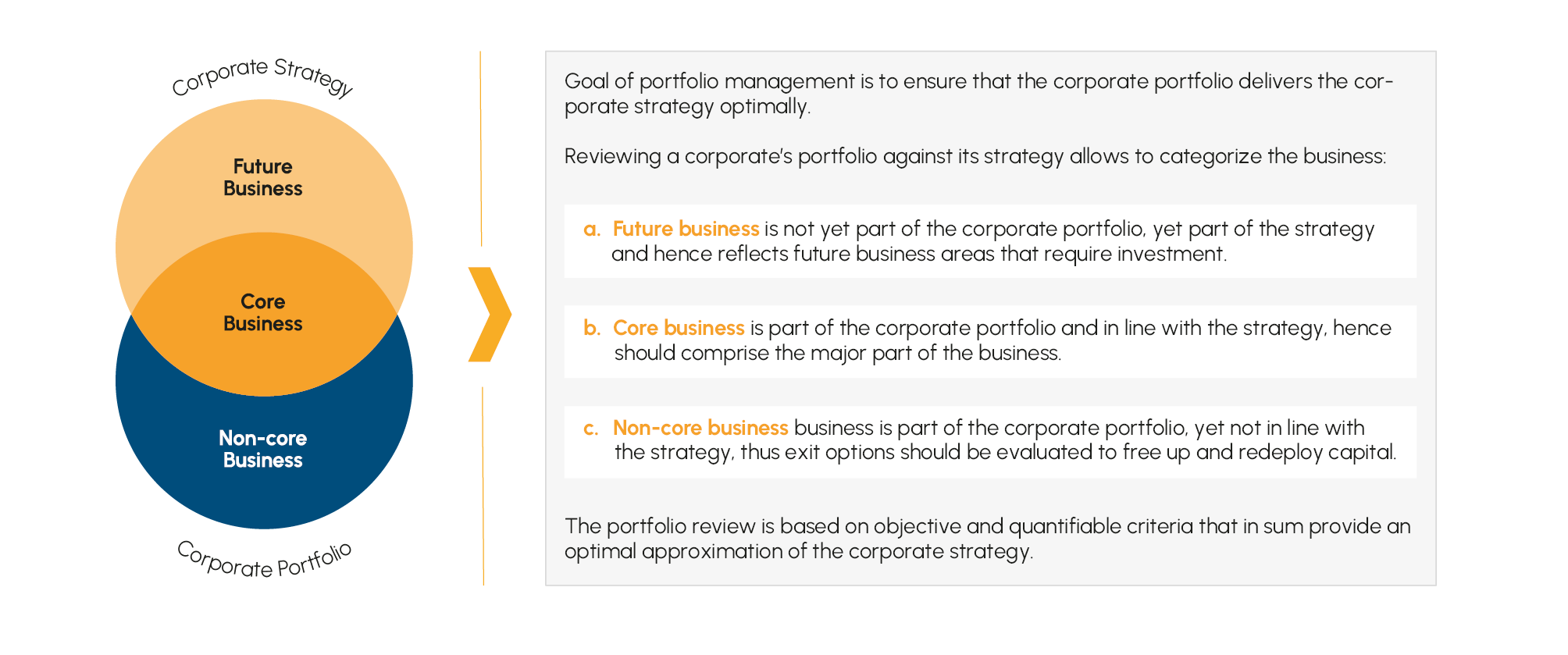

Fig. 2 Regular portfolio reviews assess how well the corporate portfolio delivers the corporate strategy

and identify strategic white spots

Source: Interpath

3. What modern portfolio management entails

In complex markets, portfolio management ceases to be a periodic planning exercise and becomes an institutionalised process. Several features define it in practice. First is a willingness to act decisively under uncertainty. Executives must accept incomplete information as the normal condition of decision-making. Waiting for full clarity is no longer viable, and the capacity to make timely, consequential decisions on an imperfect basis becomes a source of advantage on its own. This pairs with the second feature, continuous transformation. Companies must reassess strategic fit on an ongoing basis, treating acquisitions, divestitures and internal development as instruments for continuous portfolio reshaping.

Sustaining that position requires deliberate attention to flexibility and to the manner in which decisions are governed. It is about maintaining optionality and retaining divestment readiness for non-core assets, structuring integrations and separations so that alternative routes remain available. The governance model must adapt accordingly. Detailed multi-year plans give way to

Clear strategic direction and guardrails instead of detailed multi-year plans

Decentralised execution authority instead of hierarchical top-down management

This enables business units to respond quickly to shifting conditions while remaining coherent as a group. This coherence depends on combining two perspectives:

Central portfolio orchestration across portfolio balance, business maturity, risk and capital allocation

Local market intelligence and operational expertise

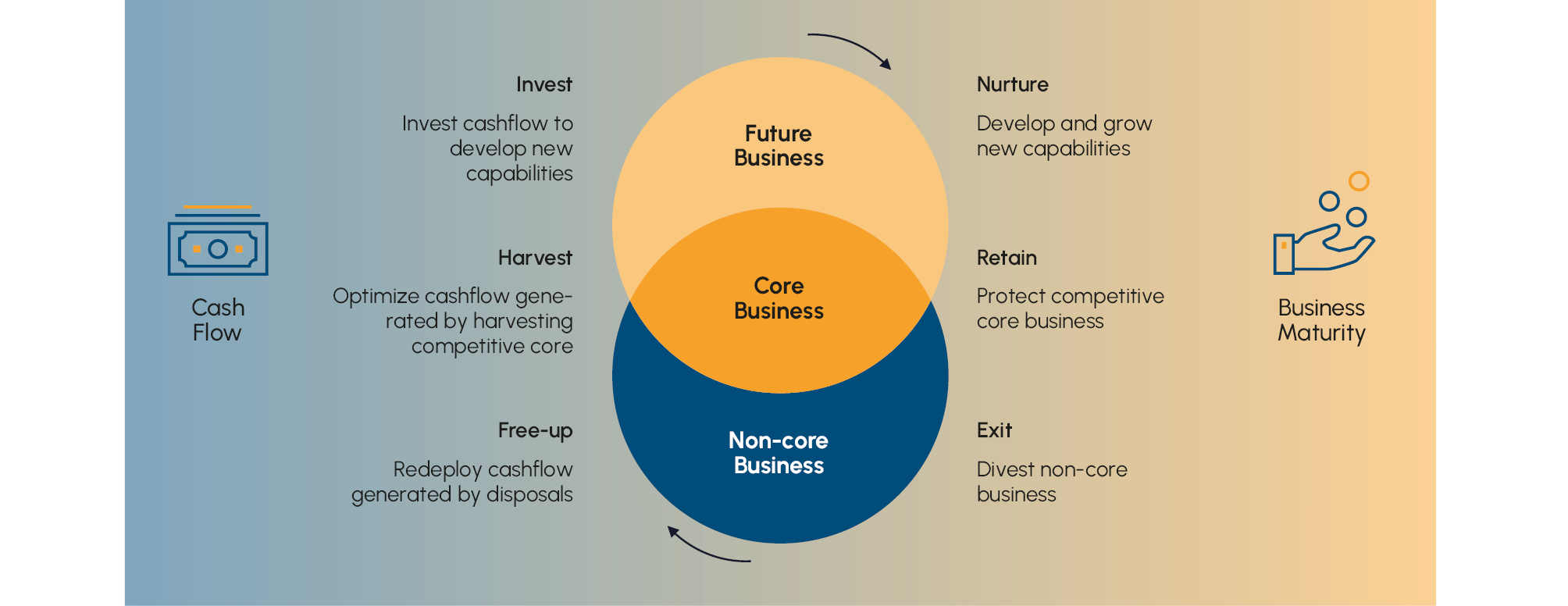

These considerations guide the composition of a portfolio. A strong portfolio is defined by its balance between risk and resilience, weighing short-term profitability and long-term growth, and evaluating existing capabilities and those the group will require in future. The most underestimated element of that balance is the continuous management of the core business. A strong core is responsible for funding future transformation and protecting its cash flows is a precondition for all future plans. However, positioning the core in a purely defensive stance is insufficient, as it must actively be adapted to remain competitive. Only by reshaping the portfolio core over time can it continue to serve as the economic engine on which future strategic direction depends.

Fig. 3 The business maturity usually evolves from future via core to non-core business and inverse to cash flows

Source: Interpath

4. The rising importance of M&A and value creation

In this environment, M&A moves from the periphery of strategy to the centre of portfolio management. Its appeal is, in the first instance, a matter of speed and scale. Compared with organic initiatives, transactions can rapidly build capability, offer instant market entry, and provide portfolio repositioning at a pace that organic development cannot match. M&A also changes the degree of change that is possible. Organic transformation is usually incremental, whereas acquisitions and divestitures enable step-change repositioning, allowing a company to enter new technologies, geographies or business models in a single move rather than over several planning cycles. It is for this reason that leading companies increasingly adopt a programmatic M&A approach, shifting from isolated, opportunistic deals toward a continuous sequence of transactions, of varying size, that enable:

Continuous shaping of the portfolio

Systematic capability building

Integrated buy-and-sell strategies

This aligns M&A directly with ongoing portfolio transformation rather than treating each deal as a one-off strategic event, adapting the target profile as consistently as the overarching strategic vision.

M&A conditions themselves have also changed, and not in the acquirer’s favour. Fewer attractive assets are available, buyers have grown more selective, and financing is tighter. Higher interest rates and reduced leverage have restricted the impact of financial engineering, making operational improvements as the primary mechanism for strong returns. This means that value creation has become the critical success factor across the entire deal lifecycle, rather than a post-deal afterthought:

Pre-deal (sell-side / separation): carve-out readiness, demonstrable stand-alone viability and a credible equity story, established before a transaction is launched

Holding period: active performance management, strategic repositioning and deliberate capability enhancement, rather than passive ownership

Post-merger integration: delivery of synergies and the alignment of cultures, operations and business models, proven in fact and not just on paper

Where such efforts are not deliberately pursued at each stage, transactions increasingly struggle to clear the return hurdles that today’s cost of capital imposes.

The uncertainty that makes M&A valuable also demands that companies and financial sponsors preserve flexibility within their holdings. Each asset should be managed so that future options remain open rather than closed off, and the conditions for continued ownership should be repeatedly tested. As conditions change, the organisation should be ready to shift between integrating, holding and selling an asset. Buying and selling cannot be siloed activities handled by different teams at different times. These are both functions of the same portfolio strategy, and managing them in unison is a defining feature of the modern portfolio.

5. Conclusion

The above outlines why portfolio management in turbulent markets is essential. The new challenge is to develop one’s capability to adapt the portfolio continuously under conditions of structural uncertainty. Moving from planning towards action by accepting the backdrop of uncertainty rather than being paralysed by it, and treating M&A and value creation as instruments of ongoing portfolio steering. Each of these shifts marks a departure from the preserver logic that served stable markets well yet serves volatile ones poorly.