Will the UK remain a major global player? A UK perspective on Global M&A

Mergers and Acquisitions (M&A) play a critical role globally as a primary, high stakes engine for corporate rejuvenation and transformation. The UK is one of the most important players in global M&A activity being closely tied to its origins and subsequent growth.

Mergers and Acquisitions (M&A) play a critical role globally as a primary, high stakes engine for corporate rejuvenation and transformation. The UK is one of the most important players in global M&A activity being closely tied to its origins and subsequent growth. M&A has a very long history in the UK, reaching back to one of the earliest recorded mergers between the East India Company, and its rival, the English Company Trading to the East Indies in 1708 to create the United Company of Merchants of England. This merged company managed to maintain its monopoly well into the 19th century1. Along with longevity of the phenomena in the UK, the country has been the second largest participant in global M&A for decades, coming second only to the USA, where both countries have dominated global deals, although more recently other countries have vied for second position. This underscores the importance M&A plays in the UK economy and its scale in global M&A activities. The UK also has a track record of innovation in M&A with the first hostile takeover in the world, by Charles Clore in 1953, to be followed by a decade of hostile bids and innovative practices in the 1980s – 1990s.2 The UK pioneered a rules based-takeover regime through the world’s first dedicated takeover regulator, the panel on takeovers and mergers, established in 1968, and a takeover code. The UK became a leader in sophisticated PE-backed take private structures and its M&A advisors were amongst the first to mainstream ESG due diligence into M&A. The combination of a long history of M&A, high volumes of deal activity, deep financial markets, sophisticated advisory systems and a track record of innovation, explain why the UK has been, and continues to be, one of the main global players in M&A today.

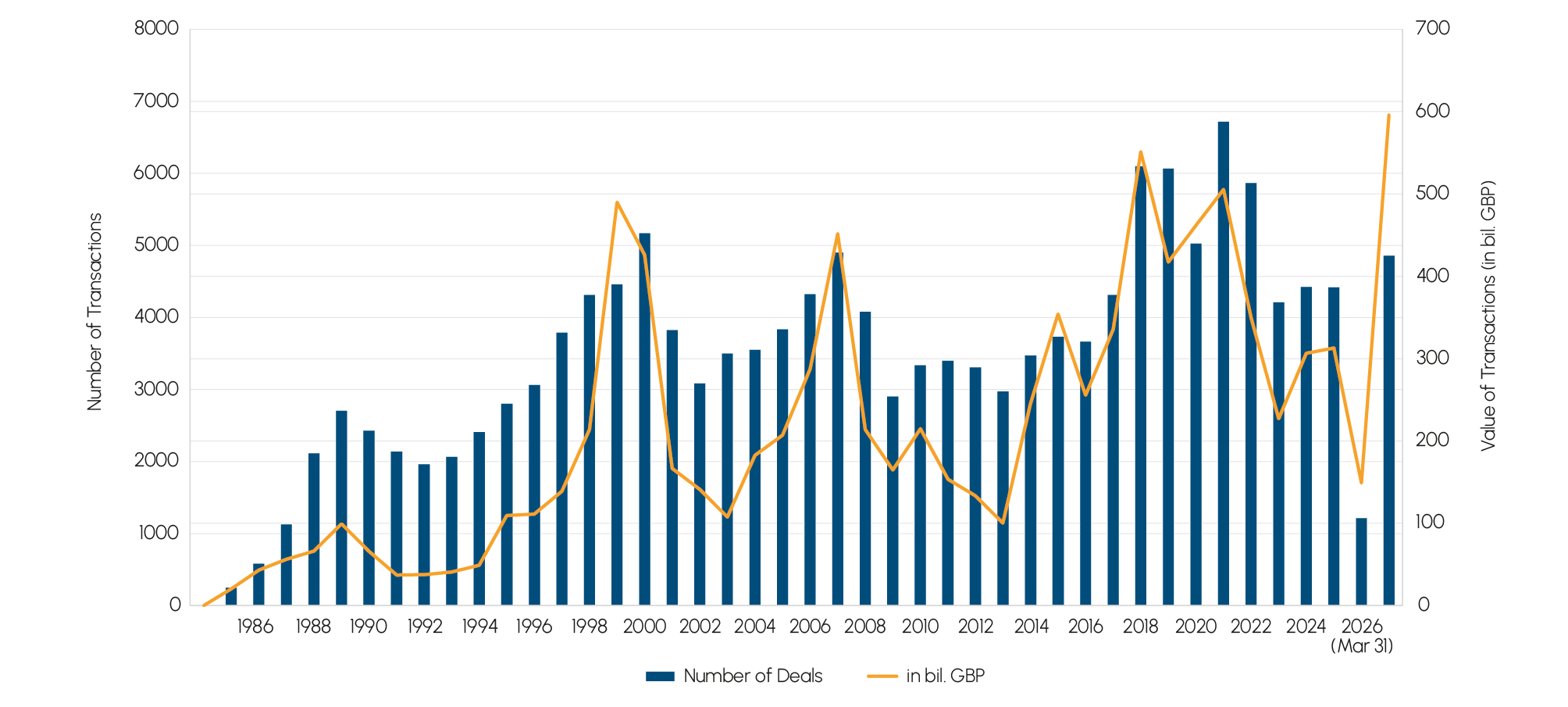

UK M&A activity has followed the broader global pattern of activity with peaks in 2000, 2007, 2018 and 2021 and troughs in 2003, 2013 and 2020, reflecting geopolitical conflict, supply chain disruption, technological disruption, and economic uncertainty (Figure 1).

Fig. 1 Mergers & Acquisitions United Kingdom

Source: IMAA (Institute for Mergers, Acquisitions and Alliances)

Source: IMAA (Institute for Mergers, Acquisitions and Alliances)

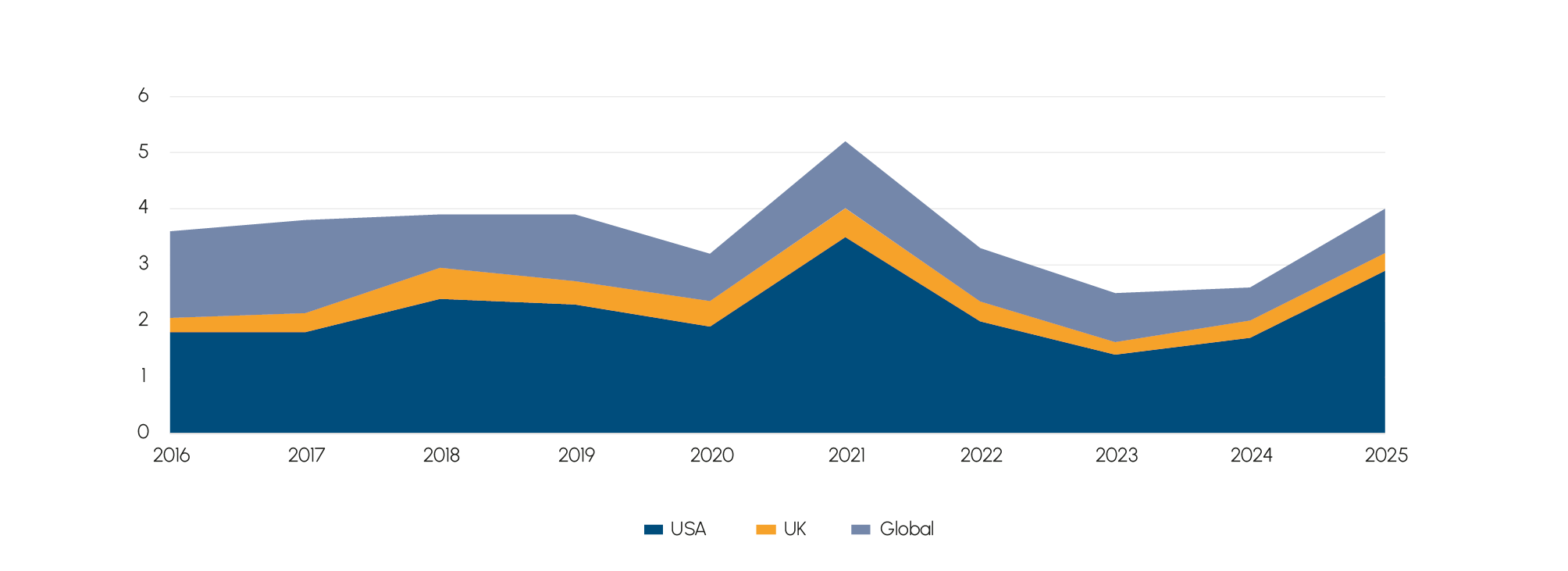

As a major player in global M&A, the UK’s M&A landscape cannot be understood in isolation from global shifts. As shown in Figure 2, UK announced deals have remained relatively constant as a proportion of global deals over the last 10 years, at approximately 11% by value and by number, although with a downturn at the beginning of 2025. Although global M&A showed recovery during 2025, in the UK deal volumes fell by 12% mirroring low growth and lack of confidence across the wider economy. Observers such as PwC3 suggest that UK M&A was characterised by fewer transactions but with significantly larger deal sizes, increasing by 28%, and higher deal values, increasing by 12%, reflecting quality over quantity.

Figure 2 shows over the last two years that global M&A has been increasingly dominated by the USA, up from its previous levels of around 60% of global totals per year to 72.5% by value in 2025. This dominance matters as the US is outperforming the UK in terms of M&A market share and advisory fees, with Wall Street Banks generating higher M&A revenues. Not only does this show greater concentration of financial power in the US but a weakening of London’s competitiveness.

Fig. 2 Global v. US v. UK announced deals ($bn)

Source: Author derived from public sources

Source: Author derived from public sources

One of the most influential factors influencing London’s competitiveness has been Brexit. The choice to leave the European Union has caused investors and businesses to reassess the attractiveness of the UK as a gateway to Europe and as an acquisition target destination. Whilst there was a short-term decline in confidence, the picture subsequently has been nuanced, partly due to the decline in the value of sterling making UK assets relatively cheaper to those in the US. However, Brexit has also made regulatory compliance more complicated where cross border deals between the UK and Europe are concerned. This has increased transaction costs and lengthened due diligence processes. Currently the UK government is making significant efforts to promote a pro-business regulatory environment for business and strengthen trading links with the EU.

In terms of target sectors in the UK, the country’s strong technology ecosystem, fintech companies and leading Universities are attractive grounds for acquiring intellectual property, digital capabilities, such as cyber security and AI expertise. Recent examples include; Swedish private equity group, EQT, bid of $12.7bn for Britain’s Intertek in 2026, a multinational Total Quality Assurance provider that operates over 1,000 laboratories in 100 countries that test, inspect and certify that products, systems and supply chains meet quality standards; the $5.3bn take-private acquisition of Darktrace, an AI and cybersecurity firm, by US private equity firm Thomas Bravo in 2024; the $3.9bn acquisition of Deliveroo, the UK food delivery platform by US company Door Dash in 2025; the acquisition of Schroders, a venerable asset and wealth manager, for $13.4bn by US investment manager Nuveen in 2026. Indeed, at the time of writing in 2026, Reuters4 has commented that there is now a rush of foreign bids for UK companies that puts Britain on track to outstrip previous records, with M&A into the country tripling to £192bn, from the same time the previous year. In addition to the Intertek and Schroder’s deals mentioned above, other notable deals include the merger of Unilever’s food division with US global flavour, seasonings and spices company McCormick for $44.8bn, and the recent $3.7bn offer for sweeteners manufacturer, Tate and Lyle by US listed global food and beverage ingredients manufacturer, Ingredion.

Outward M&A by UK firms generally operates at a lower level than inward acquisitions, although recently the gap has grown significantly, with £42.5bn inward M&A versus £16.3bn outward M&A5. The US has consistently been the largest destination for UK overseas acquisitions due to opportunities in technology and energy, the size of the market, sophisticated capital markets and shared legal and language similarities. Otherwise overseas acquisitions have tended to be in a relatively small group of other advanced economies, such as Ireland, due to closeness to the UK, strong pharmaceutical and technology sectors and tax advantages, Germany for strengths in manufacturing, engineering, chemicals and industrial technology, France for consumer brands, transport, infrastructure, luxury goods, energy and utilities, Netherlands as a European hub and home to many multinationals, Denmark and Nordic countries for strengths in renewable energy, biotech, logistics and sustainability technology, Australia for mining and natural resources, sports and financial services. Recent examples of overseas acquisitions by UK companies include GSK’s $950m acquisition of 35Pharma, a Canadian biopharmaceutical company manufacturing biologics products in 2026; GSK’s $2.2bn acquisition of US based RAPT Therapeutics, a clinical-stage biopharmaceutical company, in 2026; AstraZeneca’s purchase of US based Modella AI, a biomedical artificial intelligence company in 2026; Rio Tinto’s $6.7bn acquisition of global speciality chemicals company Arcadium Lithium, previously listed on the New York and Australian securities exchanges, in 2025.

The imbalance between inward and outward acquisitions emphasizes the attraction of the UK as a stable country with strong shareholder protections, transparent takeover rules and open capital markets. Also, the weakening of sterling has made UK assets more attractive for acquisition. This can be viewed as positive for the UK as it brings foreign investment into the country, it can support employment and innovation, save struggling firms and create shareholder gains. However, it does mean the loss of ownership and reduced control of strategic industries, although the Government has strengthened its scrutiny of foreign takeovers with the National Security and Investment (NSI) Act 2021 and through specific frameworks such as the Modern Industrial Strategy and the Defence Industry Strategy. Almost always when UK companies are acquired, the UK headquarters are relocated overseas or closed down with the loss of senior management jobs, and profits flow abroad rather than remain in the UK. Arguably a continuous imbalance of inward M&A over outward M&A can weaken the long-term development of the UK economy as domestic firms may focus more on becoming acquisition targets rather than growing into global competitors. This may be of particular concern for innovative, AI and biotech start-ups. Foreign acquirers are also likely to prioritise their global interest over national ones which could see closures, production shifting abroad, supply chains being reorganised. Nevertheless, if inward investment is productive, innovation stays strong and the domestic firm continues to grow, the net effect may be positive for the UK.

Looking ahead, it is likely the UK will remain a major player in global M&A. Despite increasing competition from New York, Paris and Singapore, London’s position as a global centre for arbitration, legal services, and international finance remains a major competitive advantage. More broadly the UK’s relatively stable legal system, sophisticated financial markets, and strong corporate governance standards continue to make it an attractive destination for international investors seeking certainty in volatile times. There are signs that confidence is gradually returning and many corporations hold very significant cash reserves that can be used for M&A. Companies also need to achieve growth which is likely to be through strategic acquisitions and they are under pressure to adapt to rapid technological changes. For the moment it is likely UK buyers will remain selective, focusing on acquisitions that offer clear technological advantages, operational resilience, or long-term strategic positioning. Whilst the UK’s structural advantages will enable it to remain important in global M&A, over the longer term the extent to which the UK’s leading position can be maintained will depend upon its ability to adapt to an evolving global M&A landscape.

1 Angwin, D. N. (2026) Origins of M&A, in Angwin, D.N., King, D., Bauer, F. (eds) (2026) Encyclopaedia of Mergers and Acquisitions, Edward Elgar Publishing. July

2 Angwin, D. N. (2026) Hostile takeovers, in Angwin, D.N., King, D., Bauer, F. (eds) (2026) Encyclopaedia of Mergers and Acquisitions, Edward Elgar Publishing. July

3 PWC (2026) Bigger bets, sharper choices: the new shape of UK M&A, UK 2026 M&A trends. https://www.pwc.co.uk/services/value-creation/insights/mergers-and-acquisitions-trends.html

4 Sakoui, A. (2026) Foreign bids drive UK M&A to new highs at $192bn already in 2026, Reuters, May 18th

5 Q3 (2024) – Q3 (2025) Office for National Statistics. https://www.ons.gov.uk/businessindustryandtrade/changestobusiness/mergersandacquisitions/bulletins/mergersandacquisitionsinvolvingukcompanies/julytoseptember2025